The next part is where it will become difficult: that is known as Business strategy Pricing (BSP), that may be a paid or a savings. 1st, the fresh new BSP might make a good bank’s mortgage provide come very appealing by allowing getting a decreased 1st interest rate.

But right here is the hook: a bank is to change new BSP at the a unique discernment loans Southside AL, considering the inner principles. Because of this that loan one to begins having low interest today becomes so much more pricey within just per year otherwise a few. It’s a critical outline to remember when you compare domestic financing choices, as possible keeps a life threatening impact on the quantity you get purchasing.

Specialist Suggestion: Even if you features home financing with an effective fixed interest, the lending company can still transform it every 2 in order to 5 years. The reason being off one thing titled a great reset clause’. Therefore, its never totally below your manage.

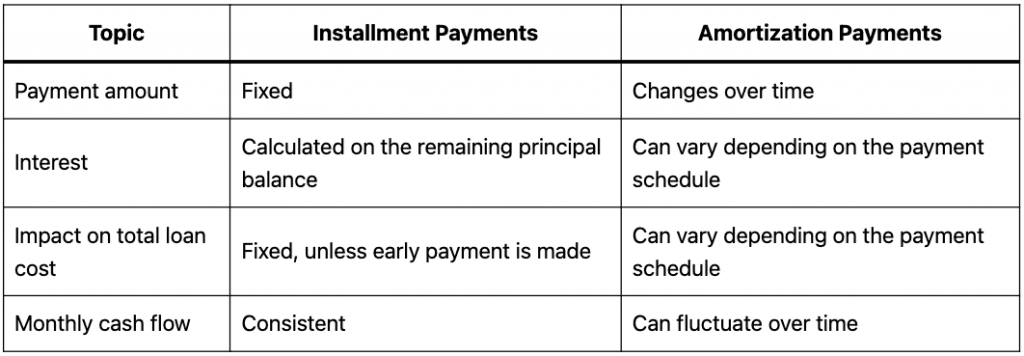

Understanding EMI: Brand new Wonders at the rear of Wide variety

Your own EMI contains several parts: the principal therefore the attention. During the early level of your mortgage, much of your EMI discusses the eye, but because you generate a lot more money, the primary begins to allege a bigger display. This is exactly titled amortization. Let’s learn Amortization with an example:

Example: Can you imagine you lent ?twenty-five lakhs at the mortgage loan out of 8% to own fifteen years. The EMI was everything ?23,891. 1st, a corner with the EMI happens towards the settling this new attention, but due to the fact go out progresses, a larger part starts reducing the dominating matter.

Remember that when interest rates change, lenders essentially expand the borrowed funds duration instead of tweaking your EMI. You actually have solutions, though: you could potentially choose replace your EMI, to change the mortgage period, or simply make up the difference during the a lump-contribution fee.

Word of new Wise: Short pre-costs to your home loan have a giant impact. They physically lower your dominant number hence saving big toward coming attract.

Your credit rating (CIBIL, CRIF, Experian etcetera.) feels as though your financial character certificate. Your credit score ‘s the big component that determines exactly how costly financing could well be to you personally. A score over 700 are favorable, however, a lowered score does not always mean the termination of the street. You continue to get that loan but from the a top rate of interest.

Just how to Improve your Credit history

step 1. Prompt Money: Try not to miss payment dates, whether it is credit card bills or any other loans. For those who overlooked one, allow it to be typical quickly.

dos. Credit Use: Staying the credit use proportion below sixty%. When you have credit cards limitation from Rs dos lacs, dont support the put restrict a lot more than Rs step 1.dos Lac for quite some time.

3. Credit Merge: Having a diverse number of credit items like playing cards, car finance, and a home loan facilitate replace your credit history.

cuatro. Old Membership: Keeping dated playing cards or mortgage accounts is very important as they create points to your credit score length.

5. New Borrowing from the bank: You should never take several the brand new credit cards or finance inside a primary period, since it adversely impacts your credit rating.

six. Argument Errors: Look at the credit rating shortly after sometime and raise a dispute when it comes down to mistake the truth is on your statement.

eight. Agreements & Write-offs: Should anyone ever choose for loan settlement otherwise have a write-away from on your own bank card, they injuries your own personal credit record permanently.

8. Secured Credit: For those who have a negative credit rating, is taking a credit card up against a beneficial FD or a little loan to create one to.